WHAT CHINA KNOWS ABOUT CSP

PaiGu/Shutterstock

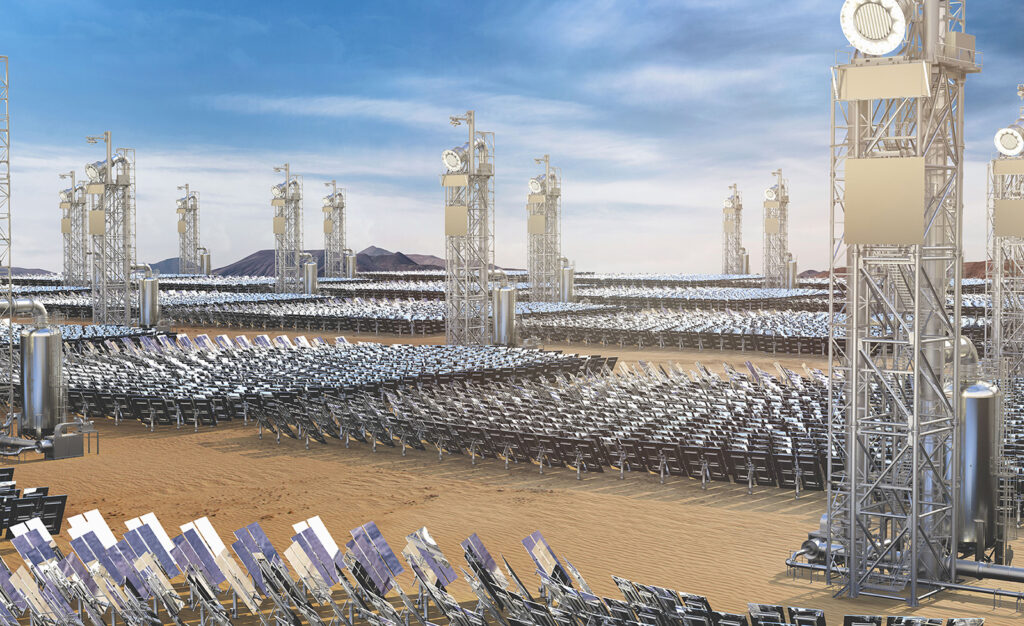

China is emerging as the only country truly scaling concentrated solar power (CSP), treating it as a strategic complement to its vast wind and photovoltaic (PV) fleets rather than a niche curiosity. While much of the rest of the world has allowed CSP development to stall, China is using an all‑of‑the‑above approach to capture CSP’s dispatchable, storage‑rich value that cannot be replicated by PV and wind alone.

Rapid CSP growth in China

China has moved from demonstration plants to a sizeable CSP fleet with a rapidly expanding project pipeline. By late 2025, analysts reported that China’s installed CSP capacity had passed 1 GW, with “a pipeline exceeding 8 GW across the provinces of Qinghai, Gansu, Inner Mongolia, and Xinjiang.” China Daily notes that between 2020 and 2024, “China’s installed CSP capacity grew at an annual compound rate of 11.7 percent, significantly higher than the global rate of 4.24 percent over the same period.”

Beijing is now locking this build‑out into medium‑term policy. In December 2025, an official guideline jointly issued by the National Development and Reform Commission (NDRC) and National Energy Administration set a target that “by 2030, the total installed capacity of CSP will strive to reach about 15 million kilowatts, and the levelized cost of electricity (LCOE) will be basically equivalent to that of coal‑fired power.”

Why CSP matters in China’s mix

Chinese planners see CSP as a system resource that solves problems created by the explosive growth of PV and wind. A SolarPACES study on China’s CSP plans noted that “CSP with heat storage can offer greater adjustability” to balance the system as variable renewables penetration rises. According to another SolarPACES analysis, “CSP is key to China meeting its climate commitments. Wind and PV are lowest c6.%09https:/www.solarpaces.org/study-csp-will-help-china-cut-costs-of-climate-action/ost, but only deliver power when it’s windy or sunny,” while CSP “with heat storage can be dispatched when needed, cutting the costs of climate action by reducing curtailment and backup requirements.”

Chinese media and officials use similar language around grid support and energy security. China Daily emphasizes that CSP’s “unique advantage of built‑in thermal energy storage… allows it to generate dispatchable power, providing grid stability by supplying electricity even when the sun is not shining, a feature essential for national energy security.” The 2025 CSP development guideline explicitly links CSP to system adequacy, calling for projects that “effectively improve the safe and reliable replacement capacity of new energy” and strengthen the “system supporting and regulating role” of CSP plants.

Global retreat versus China’s push

Outside China, CSP has largely moved from frontrunner to afterthought. The U.S. and Europe led the last CSP wave, but new build has stagnated as PV and batteries have plummeted in cost and policy support has shifted. The U.S. National Renewable Energy Laboratory’s 2025 Solar Industry Update notes that from 2004 to 2024, global CSP capacity grew only modestly and that “90% of the increase came from China, with the remainder mostly coming from Laos, Thailand, and India,” implying near‑zero net expansion in North America and Europe.

In many OECD markets, CSP has been trapped by a combination of falling PV costs, permitting challenges for large thermal plants, and the lack of coherent long‑duration storage policy. China, by contrast, has deliberately preserved the option, adopting a domestic strategy in which CSP is one tool in a portfolio of large‑scale, controllable renewables integrated through ultra‑high‑voltage transmission.

All‑of‑the‑above benefits PV and wind cannot offer

China’s all‑of‑the‑above strategy is visible in the sheer scale of its variable renewables build‑out. Taiyang News reports that by October 2025, China had cumulatively installed about “1.14 TW AC of solar energy capacity and 590 GW AC of wind,” and has set a target to reach “a combined 3.6 TW AC solar and wind capacity by 2035.” In such a system, CSP’s ability to store heat and dispatch power at will offers benefits that PV and wind alone cannot provide.

First, CSP provides intrinsic, long‑duration thermal storage. A LinkedIn analysis of China’s CSP market notes that CSP “converting sunlight into thermal energy… can be stored and used to generate electricity even during non‑sunny periods,” and that this is “especially effective in regions with abundant sunlight, like China’s vast desert areas.” The NDRC–NEA guideline explicitly calls for “high‑parameter and large‑capacity CSP plants in areas with suitable resource conditions and high demand for power and heat loads,” underscoring the technology’s dual role in supplying both electricity and process heat. PV and wind can be paired with batteries, but they do not inherently offer high‑temperature heat that can be flexibly allocated between power and industrial uses.

Second, CSP offers system‑level flexibility at scale. The 2050 high‑renewables roadmap for China notes that CSP with storage “can offer greater adjustability” than other renewables, making it valuable for “high renewable energy penetration” scenarios. China Daily similarly frames CSP as improving grid stability and national energy security by providing firm, dispatchable capacity in evening peaks when PV output collapses. This grid‑service orientation contrasts with PV and wind, which are optimized for low marginal cost energy but require additional infrastructure—batteries, demand response, or flexible generation—to deliver comparable reliability.

In sum, where many countries have implicitly decided that PV plus batteries is “good enough,” China is deliberately keeping CSP in the mix as a dispatchable, storage‑rich pillar of its high‑renewables system. That choice reflects a view of energy transition in which diversity, flexibility, and industrial strategy matter as much as the cheapest marginal kilowatt‑hour of solar or wind.

ROUND-THE-CLOCK CLEAN CLEAN ELECTRICITY AND HEAT

400kWe 247Solar Plants deployed at scale

247Solar Plants™ bridge the gap between conventional wind and solar and the need for round-the-clock utility power and industrial-grade heat. 247Solar Plants store the sun’s energy as heat instead of electricity, for 18 hours or more, at much less than the cost of batteries. No generators are required, and 247Solar’s turbines can also burn a variety of fuels, including hydrogen, to ensure 24/7/365 dispatchability.

Extensive Applications

On-grid or off-grid, 247Solar Plants offer a 24/7 alternative to fossil fuels for a broad range of applications:

- Industrial CHP: 24/7 low-carbon Combined Heat & Power for industry

- Data Centers: 247Solar’s hybrid clean solutions are ready to power your data centers as soon as you can build them. 247Solar’s solutions provide both electricity and chilling in a single turnkey package.

- Ultra Heat: Each 247Solar Plant can provide up to 1,500,000 Btu/hr. of heat at temperatures up 1000℃/1800℉ for industrial processes such as cement, glass, steel making, or minerals processing

- Microgrids: Always-on, emissions-free electricity and heat for islands, mines, communities, facilities

- 24/7 baseload power: 24/7 solar electricity, especially for emerging economies

- Green Hydrogen: 24/7 solar electricity and heat to power electrolysis around the clock

- Green Desalination: 24/7 solar electricity and heat to purify water around the clock

DATA CENTERS URGED TO BRING THEIR OWN POWER

Data center developers are being pushed to “bring your own power, or be left behind,” writes Melissa Reali in Data Center Frontier. As part of her Top 5 Data Center Industry Trends and Predictions for 2026, Reali notes how developers are turning AI campuses into integrated energy assets rather than passive utility customers. Power scarcity, new tariffs, slow interconnection, brittle equip

ment supply chains, and conditional policy incentives are converging to make self‑provisioned, often renewable, power the critical differentiator in who can actually deliver capacity. This creates opportunities for grid‑independent renewables and microgrids to emerge as practical solutions that can be deployed on data‑center timelines, not utility timelines.

Why developers can’t just rely on the grid

Reali frames power scarcity as “the defining structural limit on AI and hyperscale growth,” with U.S. data‑center load expected to nearly triple by 2030 and, in some territories, account for “more than half of forecasted demand growth.” Interconnection and grid‑upgrade delays are driven not only by permitting but also by “limited manufacturing capacity and long lead times on critical equipment,” especially high‑voltage transformers and switchgear with multi‑year backlogs.

Regulators are also shifting cost and risk onto large loads. In Ohio and parts of Virginia and Texas, Reali writes, new tariffs require big data‑center customers to accept firm‑load obligations and pay for a larger share of subscribed capacity regardless of actual usage, explicitly recognizing their grid impact. A Pennsylvania bill would require data centers to fund their own utility upgrades, previewing an expectation that operators co‑finance transmission extensions, new substations, and distribution reinforcement. These measures make it expensive and uncertain to sit in the interconnection queue and wait for utility‑built capacity.

On‑site and near‑site power: from stopgap to core strategy

In response, operators “are increasingly deploying on‑site or near‑site generation—gas turbines, diesel engines, fuel cells, and large‑scale battery energy storage—to bridge multi‑year delays in grid upgrades and interconnection queues.” Bloom Energy’s 2025 report, cited in the article, projects that roughly 30% of data center sites will use some form of on‑site power as a primary source by 2030 because grid upgrades are lagging. External forecasts go further, estimating that over a quarter of data centers could be fully powered by on‑site generation by 2030, up from about 1% today.

Reali predicts that by the end of 2026, “the most competitive AI campuses will behave less like data center loads and more like integrated energy assets, with dedicated microgrids, dispatch rights, and explicit carbon performance targets baked into financing and customer contracts.”

Renewables to the rescue

The need for self‑provisioned power aligns directly with renewable technologies that can be deployed today in grid‑independent or grid‑interactive microgrids. Modern data‑center microgrids combine local generation, batteries, and controls to “reduce dependence on centralized fossil fuel‑based power generation, increase resilience, and head off emerging community concerns of data centers’ thirst for power.”

Developers’ need to bring their own power creates a natural opening for grid‑independent renewables that can be built on the same schedule as AI campuses and integrated into microgrids. The same forces pushing data centers toward self‑provisioned energy—power scarcity, cost‑shifting tariffs, and long interconnection queues—make on‑site solar, wind, fuel cells and storage highly attractive.

Read more.

CLEAN ENERGY M&A READY TO REBOUND

Bloomberg reports that “Clean energy projects are poised for a revival in mergers and acquisitions activity due to a strengthening outlook for electricity demand and converging expectations on asset valuations.”

According to writer Ishika Mookerjee, M&A executives see potential for a fresh wave of project-level transactions as data centers and other industries support renewable energy.

This is because “asset owners are becoming more prepared to lower their price expectations,” Mookerjee says, “while buyers are becoming more willing to pay for clean energy generation capacity.”

Asset owners have struggled to complete project sales in the past year and are increasingly prepared to lower their price expectations, while buyers are becoming more willing to pay for clean energy generation capacity.

Mookerjee notes that solar, wind, and energy storage completed acquisitions of individual assets or project portfolios totaled 55.3 gigawatts of generation capacity last year, the lowest total since 2017. However, she quotes Nuveen Infrastructure’s Global Head of Clean Energy, Joost Bergsma, who says, “Slowly we’re starting to see a little bit more confidence, and also the exit market starts to be a bit more fluid in the clean energy space.”

According to Mookerjee, the International Energy Agency is forecasting renewable energy, particularly solar, to grow faster than any other major source of electricity generation through 2035. That’s being driven by an at least 40% increase in global demand spurred by adoption of data centers, electric vehicles and air conditioners.

Greg Zdun, JPMorgan’s Asia Pacific head of energy transition and natural resources, projects that as power demand, including for clean energy, “increases more than expected, we may find demand-supply tightening and a premium being paid for quality development assets.”

Read more.

FOLLOW & JOIN 247Solar

Contact: info@247solar.com